Let’s be honest: thieves of all categories simply adore trading establishments. Someone pulls a wallet out of a woman’s purse while in line, someone opens the cash register at night, or someone shovels things from the counter under their jacket. The video surveillance system will help to punish miscreants. How to make it as effective as possible?

Among the most important criteria are correctly chosen places for installing CCTV cameras. It’s one thing if you have a small shop. In this case, literally, several CCTV cameras will be enough: in the entrance-exit area and the main hall, so that the cash register and counters are visible. But if the store is a little bigger, it is worth considering all the “hot” points.

Let’s start with the most obvious:

Trading hall. If its area is large, then several CCTV cameras should be placed around the perimeter.

Cash desks, as well as checkout areas

Entrances/exits, including rear and emergency exits

Warehouses with goods

luggage storage

The area close to the store

Installation of CCTV cameras in these places is a “must-have”, and it is probably not necessary to explain why exactly. However, there are several places that are often forgotten, but which are no less important.

Ramps and loading platforms: more for personal safety, but thefts happen there too.

Entrances to service premises: the personal things of employees and store property are often the target of offenders. For example, someone can quickly grab a laptop from the office if the workplace is left unattended.

The area with ATMs, top-up terminals, coffee machines, etc.: it is always crowdy here, people stand in lines, get money, wallets… A fishy place for a thief. And a larger predatory “fish” can target an entire ATM, pretending to be a technical specialist!

Area with garbage cans: unfortunately, employees of large stores are also not very honest. Taking something expensive to the trash and then picking it up is also a working scheme.

A little general advice. In trade establishments, CCTV cameras should be installed in the most visible places. This will become a factor of passive protection. Having felt the watchful “look” of the video surveillance system, the thief will most likely change his mind about committing a crime.

Partizan video surveillance systems have been helping bring shoplifters to justice since 2008! Contact us and we will choose the best option for any task

After a string of live events in Belgrade and Zagreb which broke attendance records, Adria Security Summit Powered by Intersec 2023 goes back to the EU with a show in Ljubljana scheduled for October 25-26 2023. It’s the Summit’s second outing in Ljubljana, which is only fitting considering that it has now established itself on the roadmap of the key European industry events.

The venue is Gospodarsko razstavišče (Dunajska cesta 18), a place that will bring together leading regional and global industry leaders in the fields of security, cyber security, IoT, ICT, smart solutions, mobility, and automation.

This year, the event will put a twist on its tried-and-tested formula by focusing on innovations in the most hands-on sense – making the innovations serve the market without intermediaries by helping it take the existing challenges in stride and integrate diverse solutions into a single system that works across national legislations.

By focusing on innovation, Adria Security Summit will reinvent itself while building upon what worked for it in the past and what drew in the record-breaking numbers of attendees, sponsors, and exhibitors. This year, the projections go beyond what was achieved last year in Zagreb, so the organizers expect to see over 150 exhibitors, 3000+ visitors, 20+ event partners, 3600+ meetings, and a conference program built around panel discussions, podcasts, keynotes, case studies, startup and showroom presentations.

Speaking of innovations, Adria Security Summit will also streamline its important facet of serving as a business hub that brings together partners within and beyond the scope of industries it covers and helps them gain a foothold in the local and regional markets, propel their investments, build lasting business alliances and get to know the cutting-edge technologies.

Security cameras made by Chinese company Hikvision can no longer be installed in or on government buildings after cabinet minister Oliver Dowden declared them “current and future possible security risks”. This came after calls for a nationwide ban by a group of MPs and peers, but doesn’t go far enough, according to the UK’s outgoing biometrics and surveillance cameras commissioner.

Hikvision is partly owned by the Chinese government and is the largest CCTV provider in the world, serving schools, public institutions and secret laboratories in the UK. It supplies up to 60% of UK public bodies with CCTV cameras according to a report by Big Brother Watch, which found that the cameras from Hikvision and Dahua, another partly Chinese government-owned manufacturer, were used by 73% of local authorities, 35% of police forces and 63% of schools in the UK.

The new decision by the UK government includes a ban on the future installation of any security cameras made by companies subject to Chinese security laws and came after a review of the security risks linked to surveillance systems on the government estate.

“The review has concluded that, in light of the threat to the UK and the increasing capability and connectivity of these systems, additional controls are required,” Dowden wrote in a statement to parliament.

Over a million of these cameras are thought to be on buildings across the UK, including on government and publicly owned property.

In a statement to the media, Hikvision said it was “categorically false to represent Hikvision as a threat to national security.”

“Hikvision is an equipment manufacturer that has no visibility into end users’ video data,” the Hangzhou-based company said. “Hikvision cannot access end users’ video data and cannot transmit data from end-users to third parties. We do not manage end-user databases, nor do we sell cloud storage in the UK. Our cameras are compliant with the applicable UK rules and regulations and are subject to strict security requirements.”

The five key elements of Intersec are Commercial & Perimeter Security, Homeland Security, Fire & Rescue, Safety & Health, and Cyber Security

Event highlights forecasted regional commercial security market growth to USD 84.6 billion by 2026, at a CAGR of 6.4%.

Dubai, UAE: Security industry professionals from around the world are expected in Dubai in January to explore the strategies and advanced technologies that will future-proof global safety. More than 1,000 exhibitors from 120+ countries will unite at the 24th edition of Intersec, the world’s leading trade fair for safety, security, and fire protection. The show will take place at the Dubai World Trade Centre from January 17-19, 2023, with exhibitors providing access to more than 10,000 products across the complete security value chain.

Advanced technological innovation will dominate the exhibition’s five key segments, followed by Commercial & Perimeter Security, the second largest sector represented. Homeland security is supported by Dubai Police and Security Industry Regulatory Agency (SIRA) and is dedicated to products and solutions for Homeland Security, Law Enforcement, Airport, and Aviation Security.

Fire & Rescue will showcase the latest firefighting technologies, the best international standards, and practices, and is supported by the Dubai Civil Defence. Safety and Health will be divided into environmental, industrial, and public health and safety, and lastly, Cyber Security will host cyber solutions, experts, from national leaders to public & private sector professionals, from cyber connoisseurs to advisors, hackers to responders, and cyber economists to corporate buyers.

“We anticipate up to 30,000 security, emergency response, safety and cybersecurity professionals attending Intersec 2023, where technological breakthroughs will take centre stage and attract an influential participant profile,” said Alex Nicholl, Show Director, Messe Frankfurt Middle East. “Industry experts, influencers, decision and policymakers, and distributors are uniting to explore the strategies and technologies that will govern the safety and wellbeing of future generations.”

The event takes place against a backdrop of anticipated sector growth. Research firm 6W Research forecast the Middle East’s commercial security market will grow 16 per cent a year until 2025 to reach US$8.4 billion, while the region’s fire and safety sector will advance 7.5 per cent annually to reach US$16.76bn by 2026.

“This huge potential has attracted a line-up of leading industry heavyweights, including Honeywell, Bosh, Hochiki, Drager and AXIS Communications,” added Nicholl.

The conference think tank:

The Intersec 2023 Conference will be a think tank for future industry strategies, with four focused segments. The conference streams will feature the Intersec Security Leaders’ Summit, and dedicated seminar streams focusing on safety and health, fire and rescue, and tackling ever-growing sophisticated cyber security threats.

The 2023 Intersec Security Leaders’ Summit is a high-level strategic summit for the leaders and stakeholders of the security industry to collaborate, innovate and actively seek new technologies to meet the rapidly changing needs of the industry.

Tackling cybercrime:

The Middle East and Africa’s cybersecurity market size was valued at USD 5.92 Billion in 2021 and is projected to reach USD 19.79 Billion by 2030, growing at a CAGR of 14.35% from 2022 to 2030. The Intersec Cybersecurity Seminars will feature the latest trends, drivers, challenges and successful case studies across industries that are playing a substantial role in shaping the cybersecurity industry growth.

“The Cybersecurity Seminars will provide a platform of expertise, best practices, and solutions that cater to those working in and managing cyber defence. With key themes including resilience, risk and future-tech among others, the presents a rare opportunity for industry players to network with global CTOs, CISOs, heads of cybersecurity, and system integrators with real purchasing power,” said Nicholl.

Intersec 2023 has the support of Dubai Police, the Directorate General of Dubai Civil Defence, The Security Industry Regulatory Agency and Dubai Municipality.

2022 saw marked growth in the market for majority of the Security 50 companies in video surveillance and access control. However, the year is ending with the physical security industry dealing with issues that will point to major challenges in the year ahead.

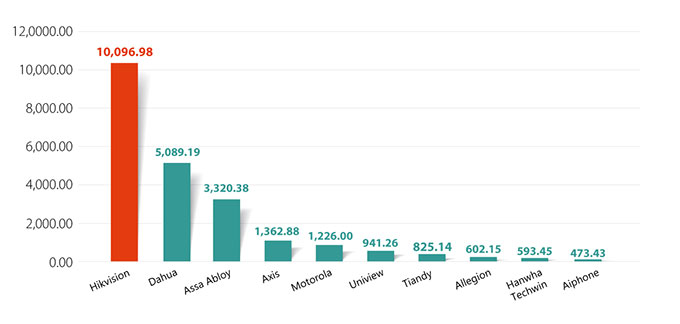

Looking at this year’s Security 50, we can see the Top 10 companies remain somewhat consistent. The top 10 biggest manufacturers in video surveillance and access control (based on 2021 revenue of security product sales) is Hikvision Digital Technology, Dahua Technology, ASSA ABLOY, Axis Communications, Motorola Solutions, Uniview Technologies, Tiandy Technologies, Allegion, Hanwha Techwin and Aiphone. Of note, Hikvision’s 2021 revenue exceeded the US$10 billion mark, standing at $10.1 billion, growing 16.9 percent from 2020’s $8.64 billion.

Security 50 2022: Top 10 manufacturers in video surveillance and access control

“We believe that technological innovation is the key element for successful development of a tech company. Our innovative technologies, products and solutions are creating values for customers, and helping many different people and types of organizations increase safety, operational efficiency and sustainability. We are glad to see that customers demonstrate long-term trust in us in return, which supports growth of the company,” said Frank Zhang, VP of Hikvision Digital Technology. “We have noticed that more external uncertainties emerged last year and this year, as inflation, interest rate hike, and exchange rate changes are affecting growth of different economies. Through optimizing our operations with enhanced flexible manufacturing processes, logistics and localized service, Hikvision has successfully maintained product delivery efficiencies. And we have kept consistent investment in technology research and development, with the R&D spending accounting over 10 percent of our total revenue in 2021. All these efforts ensured continued positive development of the company.”

Six companies are new entrants to Security 50 this year. They are: Dnake (intercom), Jovision (video) and EVETAR (lens), all from China; as well as Evolv, a U.S.-based screening solutions provider; Ava Group, an Australian risk management solutions provider; and Webgate, a Korea-based video surveillance company.

For Chinese companies, a total of 15 are in Security 50 this year. Among them, Hikvision, Dahua, Uniview and Tiandy are within Top 10. Most Chinese companies reported 2021 growth, indicating impacts from U.S.-led trade sanctions on Chinese goods were limited.

It’s interesting to note, however, that a lot of Chinese companies reported year-over-year revenue declines in the first half of this year. Hikvision, meanwhile, posted a total net profit of $848.6 million in the first half of 2022, down 11.14 percent from the first half of 2021, though its 2022 H1 revenue increased 9.9 percent y-o-y.

Yet this has more to do with China’s own domestic COVID and other issues, rather than the trade conflict itself. “Much of this is down to conditions in the Chinese domestic market rather than tariffs and trade restrictions in the US. The first half of 2022 has seen restrictions on movement in several major Chinese cities due to the COVID-19 pandemic. Government spending has therefore been diverted away from other areas and towards battling COVID-19 and supporting its economy during lockdowns,” said Josh Woodhouse, Lead analyst and Founder, and Jon Cropley, Principal Analyst, of Novaira Insights.

Speaking of U.S.-China trade conflict, all eyes are watching whether Taiwan security makers have benefited. Upon an initial look, this is indeed the case as certain Taiwan companies, including Dynacolor, Hi Sharp and GeoVision, reported good growth in 2021. Yet given Taiwan manufacturers’ smaller scale and capacity, whether they can continue to benefit from OEM orders transferred from China remains to be seen. In fact, most Taiwan manufacturers have re-strategized to make niche, value-added solutions in, for example, smart transportation, and that has been one of the contributing factors to their successes.

2021-2022 review: Growth returned to physical security market

Looking back at 2021 and 2022, indeed growth returned to security due to an easing of the pandemic. “With more availability of vaccines and treatments for COVID-19, many businesses were able to start pivoting their business strategies towards creating a safe environment for employees and customers to return to physical spaces, while also maintaining (and even expanding) the remote solutions implemented during the height of the pandemic,” said Danielle VanZandt, Senior Industry Analyst for Security at Frost & Sullivan. “For many security technology markets, spending and investment opportunities returned back to their pre-pandemic levels, with some technologies witnessing further gains due to ongoing digitalization initiatives—markets like biometrics, access control, video analytics, and digital intelligence all witnessed significant growth this year.”

Across the global markets there is a solid underlying market growth … One driver for that is the overall increasing interest in security and network video solutions. Another driver is that of technology development. The demand for our products increases as we develop new and more innovative products and solutions to address customer demands,” said Ray Mauritsson, CEO at Axis Communications.

2023 forecast: Challenges lie ahead for security industry

Just when we thought the pandemic nightmare was about to be over, a new set of challenges and difficulties have emerged, impacting various industries including security. A post-COVID surge in demand, as well as the aftermath of regional conflicts, have triggered the worst supply chain crisis in a generation. This has also partially contributed to out-of-control, across-the-board inflation in a range of areas, from energy to food to consumer products. To curb inflation, interest rates have been hiked to the highest in years, raising the spectre of recession. Indeed, the world we knew pre-COVID has changed, and, despite a return to growth in security, the above-mentioned challenges bode not so favorably for the industry in the coming year.

Supply chain issues

As mentioned, the security industry is now faced with certain challenges, one being the worst supply chain crisis in decades. “As with many other companies, we have been affected by supply chain issues. Lockdowns and other disruptions caused by the pandemic was one factor. The shortage of components, which was worsened by the pandemic, was also a major factor. Product re-designs and spot market component purchases has been two examples to minimize the effect of supply shortages. Longer lead times led to slower growth than expected in 2020 and 2021. As we now are starting to see improvements in our supply chain, we are expecting to return to double-digit growth,” Mauritsson said.

Of all the component shortages, semiconductor shortages were particularly severe. This, then, has produced ramifications for security players. “Restrictions on movement due to the COVID-19 pandemic caused a surge in demand for consumer electronics. People required laptops to work from home and for home-schooling and spent more of their income on home entertainment. All this equipment required semiconductors causing huge growth in demand for them. Video surveillance equipment vendors were just one group competing for supply of semiconductors. Car manufacturers and smartphone producers were among the other groups,” Woodhouse and Cropley said.

“As far as components, one of the hardest hit technologies was in chips for any type of processor for analytics, intelligence functions, or edge capabilities. These were high in-demand solutions from all customers, so securing components in a timely manner became a key differentiator for projects pitched and won over the last year. Security vendors who were able to diversify their supply chains to secure these components and not feel the impact of adjusted logistical routes globally found themselves to be the ultimate winners,” VanZandt said.

Inflation

Inflation is also now affecting a range of industries including security. “The price of video surveillance equipment is now being impacted by inflationary pressures in the wider economy. With utility prices, labor costs and raw material costs all rising quickly, video surveillance vendors will be forced to pass on cost increases to their customers in the form of equipment price increases. The average price of a network camera is forecast to increase in both 2022 and 2023,” Woodhouse and Cropley said.

Amid the price increase, security players had to re-strategize and think of ways to retain customers. “Inflation has caused costs to raise across the board and security technology components were not an exception to this. Many vendors and integrators did have to increase their prices in order to counter this, but they turned towards offering more flexible payment models for customers, as many projects did have longer timelines than they typically would,” VanZandt said. “Additionally, much of the industry focus has turned towards enhancing the overall customer experience including offering more personalized service models. Not only does this service-based approach fit with the overall trends of the industry, but it also helps vendors to prevent significant levels of customer churn.”

Other challenges

Geopolitical conflicts in certain parts of the world have also taken a toll on security players. “The ongoing geopolitical issues that we see is of course causing concern and uncertainty. For instance, we have, as did many other companies, suspended our business operations in Russia due to the invasion of Ukraine,” Mauritsson said.

The specter of potential new data privacy regulations globally also continues to impact many new analysis and intelligence capabilities across the security industry. “Because of this, vendors must build any new solutions with the inherent privacy features already mandated in other regions or countries or have the inherent flexibility in their solution design that they can make quick changes in order to meet any new requirements that come into play,” VanZandt said.

Growth prospects murky for physical security in 2023?

Indeed the security industry is seeing growth return this year. As for next year, things look more uncertain.

“In the first half of the year, our overseas business still maintained a rapid growth, thanks to the company’s years of deep-rooted overseas efforts. It also continued to promote business localization strategies, and improved the global supply chain and various supporting systems. Business opportunities in Asia-Pacific, Africa, Latin America, and the Middle East are relatively optimistic; but there are also regions with relatively weak growth,” said Fu Liquan, Chairman of Dahua Technology. “Looking forward, overseas businesses will continue to face regional factors, inflation and other objective conditions, but the global market is vast, with opportunities and challenges coexisting, and there is still growth potential in the long run.”

Amid the challenges mentioned earlier, there is likely to be a correction in the market, impacting growth.

“The world market for video surveillance hardware and software is forecast to grow 11.7 percent in 2022. It is forecast that economic problems will impact both public and private spending on video surveillance equipment in 2023. At the same time, inflationary pressures will persist. The world market for video surveillance hardware and software is forecast to grow 6.4 percent in 2023,” Woodhouse and Cropley said.

“While I don’t expect that 2023 will be a total downturn in overall industry growth metrics, I do expect that it will cause a market correction, where growth metrics go from their high double-digit figures, and decrease back to a more sustainable, but significant 8-9 percent year-over-year,” VanZandt said, adding while challenges remain, they also bring opportunities.

“Inflation concerns, supply chain challenges, and instability in global energy markets is all causing businesses to pause many new security investments until they can see what the final impacts could be to their budgets and bottom lines. This does offer opportunities for security vendors to work that much closer with their existing customers in order to identify ways that they can augment existing solutions already in use, giving vendors feedback on potential new features to introduce or to offer testing of new capabilities with these customers before restarting investment discussions,” she said.

As for security trends for next year, AI, edge computing, cloud and cybersecurity will continue to dominate. Meanwhile, multi-dimensional perception will be another development to look for.

“From Hikvision’s perspective, multi-dimensional perception will be another big trend that will enable the security industry going to the next level. Beyond visible light imaging, we see more perception capabilities, like radar, thermal imaging, x-ray screening, temperature measuring, humidity sensing, and gas leak detection that are being added to security devices and systems, making them more powerful,” Zhang said. “By better ‘sensing’ the outside environment, identifying events, and providing more detailed information, multi-dimensional perception creates new possibilities for video security systems to be used in ever wider scenarios and applications. We are extending our machine perception technologies to the full electromagnetic spectrum, and have developed innovative products and applications that pick up X-rays, infrared rays, millimeter radar waves, sound waves, and temperature variations.”

Top growth companies share their secrets to success

By: William Pao

Taking a look at this year’s Security 50, we can see clearly that growth has returned to the security industry. In this article we spoke with some of the growth companies to see what their secrets of success were.

In last year’s Security 50, something unprecedented happened, with more companies – 28 – reporting revenue declines than growth in the height of the pandemic. Things are different this year: a large majority of companies reported year-over-year growth in 2021 revenue, reflecting what the industry was like pre-pandemic.

“We have experienced phenomenal growth in EMEA both last year and in 2022. Still, it has been a relief for all of us in the security industry to come out of two years of COVID lockdown. Being able to meet partners and customers face to face has been vital for Milestone and our sales in the first half of the year,” said Jos Beernink, VP for EMEA at Milestone Systems.

“Our growth and profitability are accelerating right into 2022, reflecting our continued leadership in specialty RFID applications for the IoT sector. We’re growing substantially faster than any of our segments which means we’re taking share from other companies,” said Steve Humphreys, CEO of Identiv. “Last quarter our RFID revenue grew 41 percent year-over-year. Our premises business grew 20 percent year-over-year. And our total revenue increase grew 16 percent year-over-year.”

Strategizing for growth

In total, 40 companies in this year’s Security 50 reported growth last year, with 28 growing by double to triple digit. The Top 10 companies in video surveillance and access control that grew the most in 2021 were: Evolv Technologies, CP Plus, DynaColor, Webgate, Intelbras, Dongguan Yutong Optical Technology, Motorola Solutions, Gallagher, Hanwha Techwin and TVT Digital Technology.

Of note, Evolv, a provider of weapons detection security screening solutions, reported a 2021 revenue of US$21.77 million, compared to $3.92 million for 2020 and translating into a y-o-y growth of 455.98 percent, due to the company’s effort to add customers and expand into key verticals and geographic markets.

Indeed, these growth figures demonstrate security companies’ strength and resilience amid various challenges presented by COVID. So how did they do it? We spoke with some of the growth companies to find out.

Staying nimble and responsive

Staying nimble and responsive amid adversity is critical. “All told, it’s been a very interesting past couple of years, first dealing through Phase 1 of the pandemic in 2020, and then phase 2 in 2021. It was our supply chain that got us through these years. We were able to get ahead of the shutdown and pre-order 4x our general monthly orders for our main suppliers once we heard the World Health Organization was in Wuhan, China, knowing how quickly China closes when needed. Two days after our orders were placed, the shutdown happened. So having inventory was certainly a major factor, as much as having production teams willing to be in our headquarters building products for customer orders,” said Jeff Burgess, Founder and CEO of BCDVideo.

Value creation for customers

Another key to growth is value creation for customers who can continue to stick to the supplier.

“With the growth of Dahua’s AI implementation ability and its continuous effort in exploring data value, the company has gradually expanded its business from traditional security to enterprise operation and management. By helping enterprises reduce costs and increase efficiency, the value of each client has been greatly improved. The company’s arduous effort in business has promoted the continuous improvement of each client’s value, which is a significant factor that drives performance growth,” said Fu Liquan, Chairman of Dahua Technology.

According to Humphreys, a commitment to value creation is exactly the reason why the company achieved growth even amid the biggest global supply chain crisis seen in a generation.

“The reality is that supply chain shortages haven’t been this bad since 1972. The RFID industry has predominantly been dominated by companies that just want to get a simple design and then crank them out in the hundreds of millions. From a business perspective that’s never been our position, partly because that’s not where the margins are,” he said. “When we go to market, the entire arc of the whole business platform is going in the direction of higher value add solutions. We are comfortable with long sales cycles. We understand customers aren’t even necessarily going to know what they can accomplish when they start out. We introduce a highly collaborative and educational selling process with customers.”

Commitment to technology innovation

Closely related to value creation is technology innovation, which allows companies to deliver products/solutions required by users. “Identiv is designing and delivering next-generation solutions that are enabling the future of the IoT. We’re a technically deep company, which is helping us to get more market share,” Humphreys said. “Technology touches people every day and it’s at our core and that drives across the premises business and the identity business, especially in RFID. Although finding great talent across all departments is a major challenge in security, we have some of the most innovative and brilliant engineering minds in the industry working in research and development. Those engineers are making the technology more deeply embedded, leveraging it more effectively, and then making it totally pervasive so that security is all-encompassing.”

Respecting local laws and policies

For multinationals, respecting local laws and policies is key to ensuring growth in overseas business. “In the face of the current complex and changeable global political and economic environment, Dahua respects the laws, policies and customs of various countries and adopts the approach of ‘one country, one policy’ to meet the requirements of globalization compliance,” Fu said. “The company continues to strengthen the strategy for the localization of overseas employees by building an international marketing and management team as well as localized marketing and service centers to further explore the global market. Globalization and the continuous growth in overseas market will also contribute to future business growth of the company.”

Growth expected to continue

Looking into 2023, most companies expressed optimism growth will continue. “We are very bullish about the security market because AI and Machine Learning open a whole new scale of possibilities, solutions, and integrations in and beyond security,” Beernink said. “At, for example transportation clients like airports, we see that our clients are enormously challenged to keep their operations running whilst challenged on employees and being confronted with much higher passenger quantity. This as an example drives a demand for clever VMS security solutions. Security managers in our markets are challenged to do more with less resources. We at Milestone Systems have great solutions to fulfil that market trend.”

“Over the past twenty years, we have been through tsunamis, memory factory fires in Japan, recessions, and presidential elections. We have basically seen it all, so we always feel like we are ready for anything. As we continue to challenge ourselves to deliver more platforms to the market, such as the Q4 2022 release of our All-in-One NVR and Deepstor high-availability external storage, it will allow us to widen our brand globally. This is also why we are forecasting twenty-percent year-over-year growth in 2023,” Burgess said.

Memoori Research Senior IoT and Security Analyst Owen Kell shares his insights on the trends that will shape the physical security industry in the year ahead.

By: Owen Kell, Senior IoT & Security Analyst, Memoori Research

Ongoing geopolitical & trade tensions threaten to put the brakes on Chinese expansion

China’s leading video surveillance giants have become increasingly dependent on foreign markets. In terms of global revenues, giants Hikvision and Dahua Technology have retained their dominance through 2022, reporting strong overseas sales growth in H1 2022, and generating revenues of over $16.7 billion in 2021.

Their future growth is, however, threatened by a combination of weak domestic demand (largely due to the knock-on effects of the Chinese government’s increasingly controversial zero-Covid approach and resultant regular lockdowns of major cities), ongoing trade tensions between China and the West, and a weakening global economic outlook.

Tensions over alleged human rights violations and the ongoing trade war between China and the U.S. has seen continued legislative moves, new sanctions, and tit-for-tat trade barriers erected that have hugely disrupted the flow of both physical security products and key product components critical to ongoing innovation between the two nations, as well as the ability of their respective manufacturers to trade in their respective markets.

Furthermore, the recently announced US government export restrictions imposed on leading chip designers NVIDIA and AMD will stymie China’s ability to cost-effectively carry out the kind of advanced computing required to remain competitive in the fields of computer vision and natural language processing AI.

Restrictions on Chinese physical products sales to particular market verticals (or indeed a total bar on sales of all of a particular company’s technology) continue to increase not only in the U.S., but also in other Western nations, and it seems that the geopolitical and trade tensions are set to get worse before they get better.

Chinese chipmakers are not yet capable of replicating the performance of these advanced NVIDIA and AMD chips, so as a result, Chinese AI researchers may be forced to revert to using multiple lower-end chips to replicate the processing power.

AI adoption goes mainstream

After several years of false dawns and over-hype, through a series of incremental steps, AI-enabled solutions have become increasingly commercially viable in the physical security space. The pace of change over the past 12 months has been particularly remarkable, with new research papers that push the boundaries of what is possible being released on virtually a weekly basis.

We have observed significant improvements in terms of the speed, accuracy and cost of machine-learning solutions for practical applications in security-related fields including complex facial recognition, cutting-edge video surveillance scene processing, audio analytics and robotics/drones, to the extent that leading AI algorithms in several areas now far exceed human capabilities for several use cases.

While the most advanced AI relies on significant computational power and processing capability, a combination of improved edge processing capabilities at the device level and flexible access to increasingly affordable cloud-based computing resources now make accessing these innovations a viable option for many firms.

The race is now on between vendors to integrate next generation AI-enabled security functionality into end-user focused applications in a way that facilitates accessibility, practicality and ease of use for everyday security scenarios. AI is increasingly replacing the manual effort required for some roles, with data interpretation that formerly required human input now being handled algorithmically, automating processes or steps to make managing security that much easier.

For security staff, this will lead to a reduction in the amount of time spent monitoring screens or watching out for alarm notifications, and more time spent conducting higher-value work. AI will be leveraged to help analyze, evaluate and prioritize data feeds, and then provide real-time prioritization and recommendations on security issues requiring the attention of the security staff.

Making this kind of AI functionality accessible to security professionals will also require integration of AI/ML tools into existing software and platforms in a way that minimizes the need for coding or technical expertise to operate, as well as providing accessibility through multiple media including handheld devices.

While concerns over the ethical usage of AI and algorithm biases will persist, the increasing levels of integration of AI tech into all manner of everyday services and solutions (particularly into digital media generation) will lead to increasingly widespread acceptance of the technology in society as a whole.

An increasingly cyber-conscious customer base

Smart buildings are experiencing an explosion in the volume of IoT devices being deployed, as well as ever-increasing levels of convergence between IT and OT networks. These factors, combined with the growing sophistication of malicious actors and increased reliance on cloud services mean that smart buildings are becoming increasingly vulnerable to cyberattacks.

The last 18 months have seen a huge rise in ransomware attacks, as well as rising costs per incident of cyberattacks on businesses around the world[1]. All too often, IoT-enabled building automation or physical security systems have acted as the “soft underbelly” of organizational cyber defense, with multiple high-profile cases of security breaches serving to highlight the risk and vulnerabilities posed.

At the customer level, awareness of cyber risk, cost implications and even the adverse effect of cyber risks on building owners/operators’ ability to effectively insure their buildings, is steadily increasing. We have observed increasingly strict cyber policies adoption among more sophisticated clients over the past year to mitigate these growing threats, with many companies adopting a “Zero Trust” approach to network architectures, as well as continuous verification as well as investments into systems hardening.

Here again, AI will also play an increasing role – both in cyberattacks and cyber defense.

Memoori’s recent report into AI & Machine Learning in Smart Buildings found that AI tools and building blocks for launching an offensive AI-driven cyberattack have already been developed by bad actors, with several incidents identified by researchers indicating that AI had been used to execute attacks faster or to gain deeper access into a system. In terms of protecting against the threat, AI is increasingly being deployed to provide cyber-risk analytics for improving organizational resilience and understanding cyber risk by improving threat intelligence, prediction, and protection as well as enabling faster attack detection and reducing the need for human cybersecurity experts.

As demonstrable cybersecurity capability moves from being a “nice to have” to a “must have” in the eyes of an increasingly cyber-conscious customer base, security solution vendors seeking to differentiate themselves will need to invest in areas including security by design, gaining cyber certification, demonstrating cyber standards compliance, and independent testing and validation of their products to help differentiate their offerings.

Other trends to watch out for in 2023

Other trends we’re actively monitoring that we believe will continue to significantly impact the market for Physical Security include:

Ongoing global supply chain woes, which look set to continue well into 2023, impacting stock levels, price inflation and component availability.

Continued blurring of the lines between cloud and on-prem physical deployments as increasing numbers of end users embrace hybrid deployment models for at least part of their security solution.

Rising demand for security systems integration and interoperability for better reporting and control of other building/business functions for applications including occupancy analytics, energy efficiency and improving the employees or tenant experience.

The ideas presented in this article draw on the findings of several recent Memoori’s research reports into cybersecurity for smart buildings, IoT in smart buildings, and AI applications for smart buildings, and will form part of Memoori’s forthcoming annual research into the Physical Security market, due for publication in December 2022.

Novaira Insights: Video surveillance market growth continues; price has increased, too.

Video surveillance is a key element in security. So how has the video surveillance market fared recently, and how is it expected to perform in the years to come? asmag.com spoke with Josh Woodhouse, Lead analyst and Founder, and Jon Cropley, Principal analyst, of Novaira Insights, which recently released a video surveillance market report.

By: William Pao, Senior Reporter

According to the report, “The world market for video surveillance hardware and software,” the global video surveillance market grew 16.4 percent in 2021. An easing of restrictions on movement and efforts to meet pent-up demand post-COVID were cited as some of the key growth drivers. Indeed, amid project resumptions and construction booms in various parts of the world, a continuation of growth in the video surveillance market is all but expected.

Price hikes resulting from supply shortages

However, the report cited the global average price of a network camera increased by over 7 percent last year, making 2021 the first year in which the global average price of a network camera increased rather than decreased. A main reason cited by the report was a shortage of components used for production of video surveillance equipment, resulting in higher prices for those components; this then forced video surveillance equipment vendors who were unable to absorb such cost increases to raise the prices of their own equipment.

Especially, vendors were faced with a shortage in semiconductors, which are the basis for image signal processors and SoCs that are key components in IP cameras.

CHIP Act may help somewhat, but not in short term

“A shortage of semiconductors was particularly problematic. However, there was also shortages of resistors and materials such as some plastics and metals,” Woodhouse and Cropley said, adding that the CHIP Act recently signed into law in the United States may improve the chip shortage situation somewhat, but not anytime soon.

“It is likely that the CHIP Act will lead to greater production of semiconductors in the U.S. in the longer term. However, it will take years for new production facilities to be built and for volumes to ramp up. The impact of the CHIP Act is therefore likely to only start being felt towards the end of the forecasts in our report (our forecasts run to 2026),” Woodhouse and Cropley said.

According to both, general inflationary pressures will force vendors to increase prices yet further in 2022 and 2023. This, then, is expected to produce an impact in the video surveillance market. “SIs and end users will purchase fewer surveillance cameras than they would do if prices weren’t rising. This will mean that camera unit shipment growth will be lower in 2022 than it was in 2021. Growth will then be even lower in 2023 than it was in 2022,” Woodhouse and Cropley said. “The global average price of a network camera and an analog camera is forecast to fall again in 2024. However, a more prolonged period of high inflation presents a serious risk to this forecast.”

As for next year, the report said the global video surveillance market for hardware and software is forecast to grow at 11.7 percent in 2022 and will be worth an estimated US$28.2 billion. “We are forecasting much lower growth in 2023 followed by gradual recovery with growth increasing from 2024 onwards,” Woodhouse and Cropley said.

Cloud adoption increases, especially in U.S.

Technology-wise, a gradual trend to using the cloud for video surveillance also continued in 2021, particularly in the Americas region where the market for cloud video management software exceeded $150 million, the report said. It forecasts the number of cloud-connected surveillance cameras in the Americas will grow on average over twice as quickly as new network camera shipments between 2021 and 2026.

Especially, the report found the United States has been quicker to adopt cloud for video surveillance than most other countries in the world. Woodhouse and Cropley explains why this might be.

“It is down to a mixture of factors. A major factor is that it has many organizations with distributed sites, each with a small number of cameras. Furthermore, these organizations operate in a large country using a common language and a common set of rules on data residency, privacy etc. Bandwidth availability and cost have been more favorable than in some other countries too,” they said.

OSSA: Orchestrating the Digital Data Flow

Open Security & Safety Alliance (OSSA), a collaborative initiative focused on creating a framework for standards and specifications in the security, safety and building automation space, shares their thoughts on the unfolding trend that will change the security industry in the year to come.

By: Gijs van den Heuvel, Chair of Marketing at the Open Security & Safety Alliance (OSSA) and Manager Strategy and Partner Collaboration at Bosch Security Systems

As an industry alliance, we have a good idea of what’s in the works by our members when it comes to innovating across important areas within security, safety and beyond. OSSA representatives hail from some of the most influential companies in this space – such as Bosch, Hanwha Techwin, Milestone Systems and VIVOTEK – and together are determined to continue bringing forth an open, data-driven ecosystem.

The IoT is all about connecting things to make life easier, more intelligent, more intuitive and more productive. OSSA workgroups have projects underway that are primed to unify and elevate the market as a whole, so that there will be headspace to grow for all participants.

Already, OSSA organizations specified hardware and software conditions to make it possible to run third-party (AI) analytics applications securely on existing, brand-agnostic computer vision devices (starting with cameras). Working together spurred a handful of specifications for building common components (e.g., for core system requirements, cyber security directions and application interface APIs) that can be utilized jointly.

Now, a notable future trend our members are funneling expertise into is bringing about new levels of data and information sharing to all we do when it comes to smart cameras and related IoT devices. How can we achieve next-level dissemination of extremely valuable data flows sensed by products that collect data in their brand-specific siloes? How do we establish open but secure pathways to easily share and uniformly interpret data to connect the dots when it comes to surveillance and activities being captured and contained on edge-computing devices?

Millions of “things” generate, accumulate and house heaps of factual insights that – unfortunately all too often – remain untapped and stagnant once recorded. If corralled, connected and optionally given an artificial intelligence/ML scrub, this information brings a bigger picture of what transpired across, for example, surveillance systems. Taking frames or moments from various devices and drawing relationships between them to form a cohesive “data flow” opens up a massive new corridor of IoT-based possibilities. According to our group, there resides tremendous value in making data from one source consistently interpretable for another.

Imagine harnessing content from a camera that captures a car and applies its license plate app to read the details. This car crosses in front of the building, and minutes later another camera across the facility records an individual scaling a fence in the vicinity where the car was last detected. Finally, a third camera on the opposite side of the building records an individual onsite in an unauthorized area, and an open platform app detects a gun in hand. The system immediately then alerts security personnel about a potential threat. Tying this crucial information together seamlessly across a natural path of data flowing from security and safety devices takes us to a new frontier delivering not only what’s “seen” but more importantly what’s “sensed.” This is the future if device manufacturers and other stakeholders participate in an industry-driven ecosystem.

OSSA members are working on a set of generic, vendor-neutral data Application Programming Interfaces (APIs) to enable this type of uniform consumption and data interpretation across cameras or computer vision gateways in adherence with OSSA standards. It is also designed to apply across other device types within the IoT security and safety domain to provide a loose coupling between any pair of send/receive applications that collect, digest and interpret data. Enabling content from various brands and device types to be interpreted in an open forum brings newfound levels of storytelling and safety to our security situations.

Coupled with progress that continues around allowing for easy integration of third-party AI analytics applications on “Driven by OSSA” video cameras and gateways in an agnostic fashion, OSSA facilitates cooperation on many levels. There’s a front-row seat for anyone interesting in expanding this collaboration framework to together lift our industry to new levels of openness, innovation, interoperability and success.

London – December 2022: A recent Future Forum survey found that 58% of knowledge workers already follow a hybrid work pattern: “Flexibility is the expectation — and increasingly the norm,” the report concludes*. Further growth in flexible working is a certainty. These changing work patterns make flexibility in security ever more critical. Choosing the right access control solution will make a big difference.

Office-based working, telecommuting, work-from-home (WFH), co-working spaces and hotdesking: All these habits and schedules are now part of the mix, almost everywhere.

As the fixed “working day” declines, people come and go at different times, with changing schedules, irregular patterns and a mix of different places where they work. This presents a challenge which many existing access control systems and workflows were not built to meet.

Many of the old certainties are replaced by questions. How can I now ensure the right people — and only the right people — get seamless access when they need? How do I foster a sense of comfort and safety among workplace users — and peace of mind for the facility managers — even as people come and go in less predictable day-to-day patterns?

The role of access control: same demands, new challenges

Access control has always been critical for building security. Changing work patterns, however, mean monitoring and filtering who can go where — and at what times — is becoming even more essential. They ensure staff and visitors move safely and conveniently into and around the workplace.

Mechanical lock-and-key security has established centuries of trust. It works. But it is neither flexible nor intelligent enough to meet these new challenges.

Electronic access control, on the other hand, has this flexibility. And the quickest way to implement it — to enable a fast, efficient move to secure hybrid working — is wirelessly.

The wireless advantage for modern workplaces

The control enabled by wireless, battery-powered door locks managed by intuitive software gives facility managers the power to issue more fine-grained access permissions. Employees, contractors, cleaners, event attendees and visitors can all get the access they need — no more and no less.

Credentials may be programmed to unlock doors during specific timeframes, so staff enter only when scheduled, for example. Facility managers can regulate daily access to keep building occupancy within capacity.

Last-minute or emergency changes to access rights are no problem, because credentials have flexibility that mechanical keys do not. With the remote management functionality, office managers can perform any operation remotely, even if they are away from the premises. In case of an emergency, they could lock or open doors remotely, for example.

Mobile credentials offer even more: They can update over the air in an instant, via software which can provide control in real time, from anywhere and around the clock.

“An access system which offers this degree of control, and more, is much easier to adopt than many business owners and managers imagine,” says Mikel Gaztañaga at ASSA ABLOY Opening Solutions.

“It can provide the backbone for more efficient management of people and their security as work becomes more flexible. The right solution should also integrate with important flexible office services like support ticketing, room bookings and more.”

Wireless, battery-powered devices are fast to install and run without any mains connection. They are easy to retrofit without damaging walls and use little energy during use, unlike equivalent wired doors. Their cost-effectiveness enables fitting at many more doors than would be feasible with any alternative solution.

Flexible access control required for a flexible co-working space

In the co-working sector, flexible access to offices is a priority. As “fixed” space rented by corporations begins to fall, co-working spaces are expected to keep growing. In one recent survey, 69% of large companies “identified flexible office space as the most in-demand amenity of the future”**.

To stand out from the competition, the founders of ULab in Alicante wanted the latest in security, accessibility and design to create their 21st-century business centre***.

Flexible and wire-free, a SMARTair® system gives ULab real-time access control via credentials which are easy to program and reprogram. ULab managers chose Openow™, the Mobile Key solution for SMARTair. It gives workspace residents an option to carry virtual keys on their smartphone. It’s slick, efficient and gives ULab users and managers even more flexibility.

SMARTair software manages access for ULab’s 100 daily users. They also have the flexibility to welcome many more visitors when the event space is full.

“In addition to regular daily traffic, weekly traffic can almost multiply by 10 if an event is held,” says Enrique Burgos Pérez, Director at ULab. “We needed an access control system as flexible and convenient as SMARTair.”

London, November 2022 – Facilities and security managers, architects, building managers and many others can benefit from the time-saving support provided by a BIM and specification partnership. A webcast on December 8th introduces the process for a non-specialist audience — and explains how partnership frees up time and reduces project costs.

“No prior expertise is needed,” says Marc Ameryckx, BIM Development Manager at ASSA ABLOY Opening Solutions EMEIA. “That is the main message of our next webcast.”

From doors and door closers to wireless electronic access control, ASSA ABLOY has solutions for almost any building or opening. “This range gives us uniquely broad-based knowledge about standards and certifications,” explains Mark.

During the webcast, experts from ASSA ABLOY Opening Solutions will explain how their knowledge can help all building stakeholders — from architects to facility managers — to save time and money in building specification.

“Leaning on our expertise streamlines project management for both new-builds and retrofits. Our partners deliver faster, better and more cost-effectively.”

The value of a specification partnership

Specifying door and security solutions can be complex and time-consuming. Partnering with an expert helps architects, facility managers and other stakeholders complete their projects more time- and cost-efficiently.

When they choose ASSA ABLOY, architects enjoy personalized support from a dedicated, locally based specification team. It frees up designers’ time to focus on their core task: delivering their vision for the finished building.

ASSA ABLOY specification experts help ensure issues around fire safety and barrier-free accessibility are built into designs as early as possible. Because teams are based across ASSA ABLOY’s global network, they bring expertise on local issues, standards and certifications — and can attend in-person project meetings.

In addition, ASSA ABLOY offers in-depth support for six global green building certifications: BREEAM, LEED, Green Star, WELL, DGNB, HQE*.

Understand benefits over the full building life-cycle

The advantages of a BIM and specification partnership extend beyond the design and build stage. It also creates a legacy store of knowledge which benefits facilities management, health and safety, maintenance, refurbishment and more over the lifetime of the building.

The webcast — which is free to attend — will introduce stakeholders to these benefits in an accessible, non-technical way.

“Our expertise in every solution around the door helps to simplify some of the most painful processes in building design and management,” adds Mark.

“The main motivation for this webcast is to show non-specialists how they will really benefit from partnership with a specification expert.”

MOBOTIX AG confirms that all MOBOTIX products and systems comply with the requirements of the United States National Defense Authorization Act (NDAA) and are 100% NDAA-compliant.

The NDAA Section 889 contains a new set of guidelines that allow for increased protection against espionage and hacker attacks. In addition, there are named Chinese companies that produce components used for telecommunications purposes, (including security products) that will be no longer be acceptable.

For clarification purposes, MOBOTIX does not use any SoC (System on Chip) or any other components that are capable of processing software from Chinese companies. Furthermore, MOBOTIX products that are sourced from its OEM partners (Original Equipment Manufacturers) are also 100% NDAA compliant. MOBOTIX has clearly demonstrated a defined 3-step self-certification process that its products and systems do not contain forbidden components.

“MOBOTIX technology is not only a world leader from a quality perspective, but also from a data and cyber-security perspective. It has always been extremely important for us not to use components from risky suppliers to protect the security of our customers and partners through our own design.” explains Hartmut Sprave, CTO of MOBOTIX AG.